Bike Theft Tracking Devices and Insurance: A Rider’s Guide to Staying Secure

You lock your bike. You double-check the lock. You walk away, but that nagging feeling? Yeah, it’s still there. Bike theft is a gut-wrenching reality, and honestly, it’s getting worse. But here’s the thing—technology has finally caught up with our paranoia. Tracking devices and insurance aren’t just add-ons anymore; they’re a lifeline. Let’s break down how these two work together, and maybe—just maybe—you’ll sleep a little easier tonight.

The Cold, Hard Truth About Bike Theft

Every year, over 2 million bicycles are stolen globally. That’s not a typo. And recovery rates? They hover around 5%. Brutal, right? But here’s where tracking devices flip the script. They don’t just hope your bike comes back—they give you a fighting chance. Think of them as a digital bloodhound, sniffing out your ride even when it’s hidden in a shipping container or a sketchy basement.

Insurance companies have noticed this shift. Some now offer discounts if you install a tracker. Others require it for high-value bikes. So, it’s not just about recovery—it’s about reducing risk and maybe saving a few bucks on your premium.

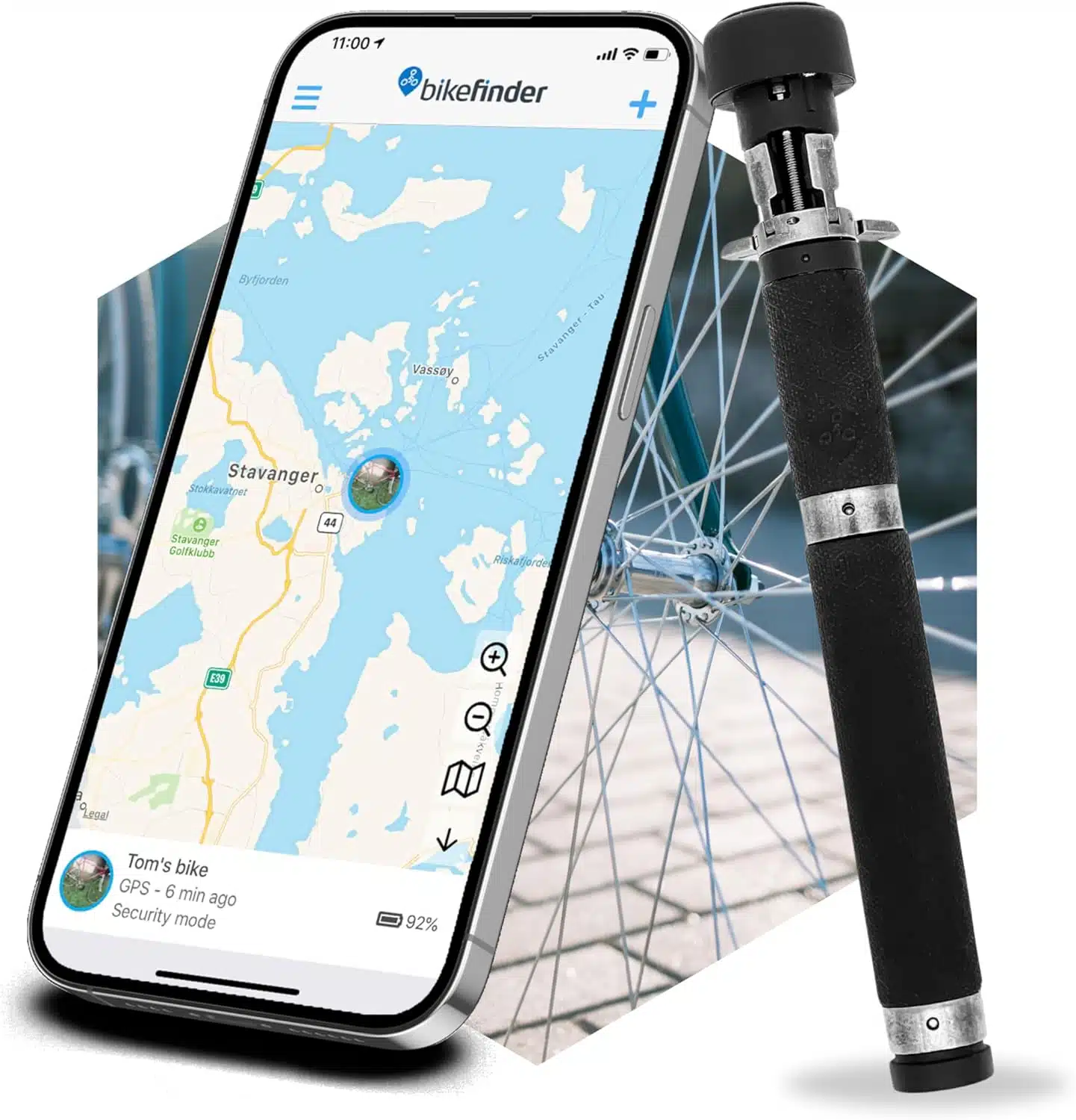

How Tracking Devices Actually Work (No Jargon, Promise)

Most trackers use one of two technologies: GPS or Bluetooth. GPS is the heavy lifter—it uses satellites, so it works anywhere. But it drains batteries faster and often requires a subscription. Bluetooth, on the other hand, is cheaper and lasts months on a single coin cell. The catch? It only works within a 100–300 foot range, relying on a community network (like Apple’s Find My or Tile’s crowd-sourcing) to ping its location.

Here’s a quick comparison:

| Feature | GPS Tracker | Bluetooth Tracker |

|---|---|---|

| Range | Global (via cellular) | ~300 ft (crowd-sourced) |

| Battery Life | Weeks (rechargeable) | Months to a year (replaceable) |

| Monthly Fee | $5–$15 | Usually free |

| Best For | High-end bikes, long-term recovery | Commuter bikes, quick alerts |

Personally, I’d recommend a hybrid approach—use a hidden GPS tracker for the big stuff, and slap a Bluetooth tag under your seat for daily peace of mind. But hey, that’s just me.

Insurance: The Safety Net You Didn’t Know You Needed

Standard renters or homeowners insurance might cover bike theft, but it’s a minefield. Deductibles are often high, and depreciation hits hard. That $2,000 carbon fiber frame? You’ll get maybe $600 after depreciation and the deductible. Ouch.

That’s where specialized bike insurance shines. Companies like Velosurance, Markel, or even your local broker offer policies that cover replacement cost—not depreciated value. Some even cover accessories, race fees, and rental bikes while yours is in the shop. And here’s the kicker: many insurers now ask, “Do you use a tracking device?” If you say yes, your premium drops by 10–20%. It’s like getting a discount for being paranoid. I’ll take that.

What to Look for in a Bike Insurance Policy

- Replacement cost vs. actual cash value – Always pick replacement cost if you can swing it. Your bike’s value drops faster than a rock.

- Worldwide coverage – If you travel with your bike, make sure theft is covered abroad. Some policies exclude “unlocked” bikes, even in a hotel room.

- Deductible amount – Lower deductibles mean higher premiums. Find a sweet spot. $250 is common.

- Accessories and upgrades – That new saddle, those carbon wheels? Make sure they’re itemized. Standard policies often cap accessory coverage at $500.

Pro tip: Read the fine print on “negligence.” Some insurers won’t pay if you used a cheap cable lock. Others require a specific grade of U-lock. It’s annoying, but it’s reality.

Pairing Trackers with Insurance: The Perfect Marriage

Think of it this way: a tracking device is your detective, and insurance is your safety net. Together, they cover the two worst-case scenarios—finding your bike and replacing it if you can’t. But they work best when you’re proactive.

For instance, if your bike gets stolen and you have a GPS tracker, you can provide real-time location data to the police. Some insurers even have partnerships with recovery services. Velosurance, for example, works with a company called Bike Index to log serial numbers and track stolen bikes. It’s a small step, but it builds a paper trail that speeds up claims.

And here’s a weird quirk: some insurers require you to report the theft within 24 hours. If you have a tracker, you can do that instantly. Without one? You might spend days scouring Craigslist and Facebook Marketplace. That delay could cost you your claim.

Real Talk: Do Trackers Actually Help Recover Bikes?

Short answer: yes, but with caveats. GPS trackers have a higher success rate—around 60–70% recovery in some studies. Bluetooth tags? Lower, maybe 30–40%, because they depend on other users’ phones. But that’s still way better than the 5% average. I’ve heard stories of people tracking their bike to a storage unit, calling the cops, and getting it back within hours. It’s not a guarantee, but it’s a massive edge.

One thing to watch out for: jammers. Thieves are getting smarter. Some use GPS jammers or simply remove the tracker. That’s why hidden placement matters—inside the seatpost, under the bottom bracket, or even inside a false water bottle. Out of sight, out of mind… until you need it.

Current Trends: What’s New in 2025

The market is shifting fast. Here are three trends worth noting:

- E-bike specific trackers – With e-bikes costing $3,000+, companies are building trackers that integrate with the bike’s battery. No extra charging, no bulky add-ons.

- AI-powered alerts – Some trackers now use motion sensors and AI to detect tampering. If someone lifts your bike, you get a push notification before they even cut the lock.

- Blockchain for ownership – A few startups are using blockchain to create tamper-proof ownership records. It’s early days, but it could make reselling stolen bikes nearly impossible.

Insurance companies are watching these trends closely. Some are already offering lower rates for bikes with blockchain-registered serial numbers. It’s a bit futuristic, but it’s happening.

Practical Steps to Protect Your Ride Right Now

Let’s get actionable. Here’s a quick checklist:

- Buy a tracker – Start with a Bluetooth tag (like an AirTag or Tile) if you’re on a budget. Upgrade to a GPS tracker for high-value bikes.

- Hide it well – Don’t just stick it under the saddle. Get creative—inside the handlebar, taped to the frame’s internal cable routing, or in a custom 3D-printed bracket.

- Register your bike – Use Bike Index or Project 529. It’s free, and it links your serial number to your contact info.

- Review your insurance – Call your agent. Ask specifically about bike theft coverage, deductibles, and tracker discounts. If they sound confused, shop around.

- Take photos – Document every scratch, every component. It helps with claims and with identifying your bike if it’s recovered.

And one more thing: don’t rely on just one layer. A tracker without insurance is a gamble. Insurance without a tracker is a slow, painful process. Together? They’re a system.

The Emotional Side of Theft (Yes, It Matters)

Losing a bike isn’t just about money. It’s the freedom, the commutes, the weekend rides—they vanish in a moment. I’ve had friends who stopped cycling entirely after a theft. That’s the real cost. A tracking device and insurance won’t erase that feeling, but they give you a path forward. You either get your bike back, or you get a check. Either way, you’re not stuck in limbo.

Think of it like a seatbelt. You hope you never need it, but you’d feel stupid driving without it. Same logic applies here.

Final Thoughts: Don’t Let Theft Steal Your Joy

Bike theft is a pain—a predictable, frustrating pain. But you have tools now. Tracking devices give you eyes on your bike, even when you’re miles away. Insurance gives you a financial reset button. Use both. Not because you’re paranoid, but because you love riding. And that love deserves a little backup.

So lock up. Slap on a tracker. Call your insurer. Then ride without that knot in your stomach. It’s worth it.